PROJECT LEDGERFALL: The Final Phase

(Aleksander Grandwileski),

On June 11th, 2025, one of the most powerful financial institutions in the world made an announcement that barely made a ripple in mainstream news.

But among the investors, traders, and bankers who move billions of dollars across borders every day... it sent a crystal-clear signal.

The endgame is here.

I call it Project Ledgerfall.

And it represents the final phase of a plan inside the traditional banking system that most people don't even know exists.

The Bank for International Settlements has publicly declared this project is well underway.

The Financial Times is calling this blueprint "the end of privacy."

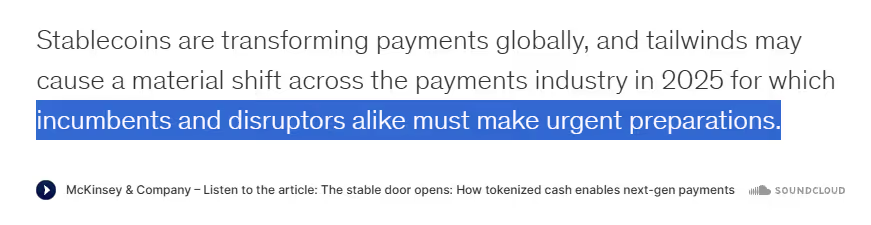

And consulting giant McKinsey is warning all savers and investors they need to make urgent preparations for the coming change.

- This isn't another digital payment upgrade.

- This isn't a minor policy shift.

- This is the missing piece.

The final step in a meticulous, three-phase masterplan that has been unfolding since the very first banks opened their doors hundreds of years ago.

And right now, in 2026, the man positioned to pull the trigger is ready to do exactly that.

First, a quick note on who I am and why I’m sharing this with you.

My name is Alex.

But most people call me The DeFi Doctor.

I started my career in medicine.

I graduated in the top 5% of my class.

I spent years working in hospitals across three countries.

But I walked away from the medical field after seeing first-hand how institutions are designed to keep people dependent, not informed.

Big Pharma.

The insurance system.

The revolving door between regulators and the companies they regulate.

I was done with systems built to exploit ordinary people.

And when I discovered a financial revolution happening right under Wall Street's nose…

…Where for the first time in history, everyday investors could access the same tools and opportunities once reserved for the elite…

I went all in.

I spent the last decade figuring out what works and what doesn't.

Teaching others how to protect themselves from institutional corruption.

Helping people build financial sovereignty outside the traditional banking system.

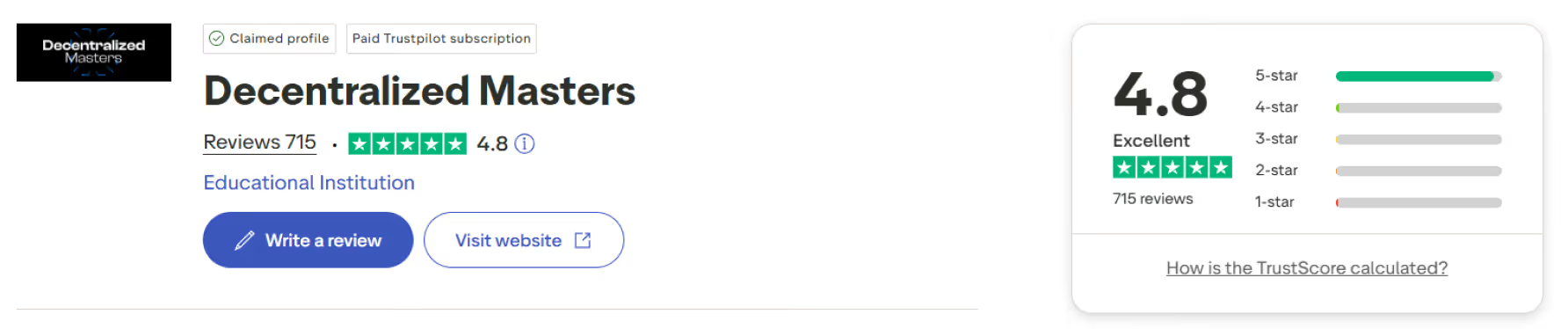

Today, I'm Head of Education at Decentralized Masters - a private community of over 4,000 serious investors with a combined net worth exceeding $4 billion.

We carry a 4.8-star rating on Trustpilot with over 600 reviews.

And a German wealth management firm (regulated by Germany's federal financial authority) recently audited our full track record.

The Results Our Members Are Seeing Right Now

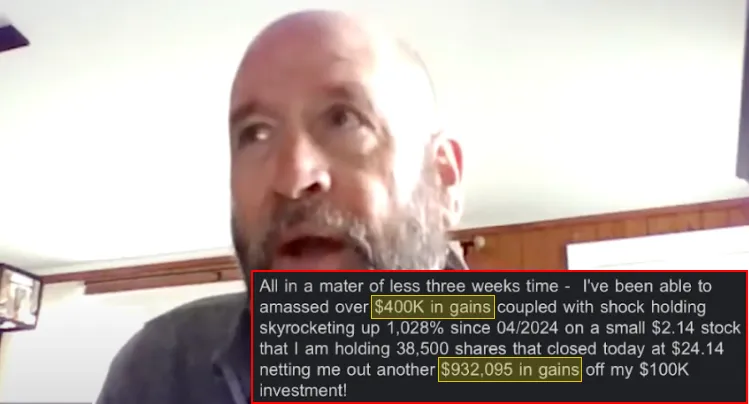

Members like Bill have put that track record to work.

He’s up $932,000 following this exact system.

Another member, David, had never touched a digital asset before joining us.

He made $27,000 in his first two weeks. Almost completely passively.

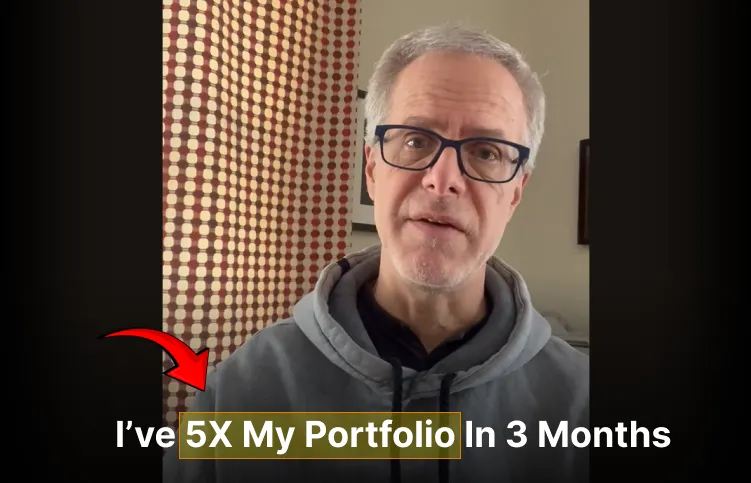

Members like Jeff are up 100k with this exact system, and especially taking advantage of the LAST PHASE of our system.

He’s 5X’ed his overall investment with us.

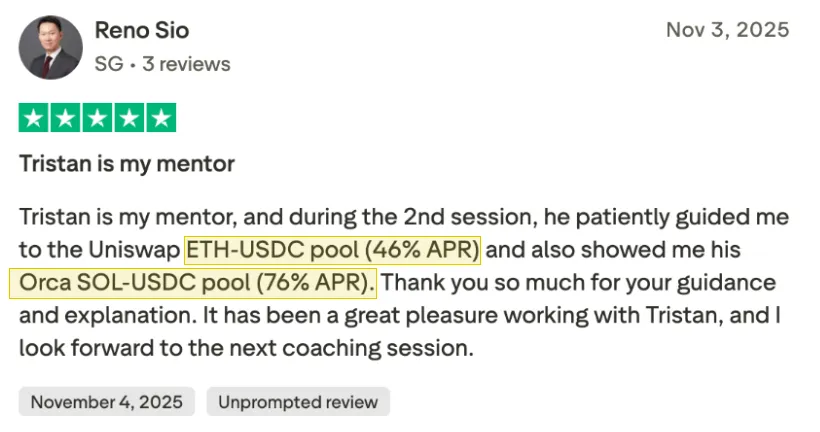

We’ve also seen many members up in market downturns… like Reno.

46% and 76% APR - and notice WHEN he wrote that review - November 3rd - while Bitcoin was falling. The market was red. Yet he’s thriving.

I could go on and on… we have 640+ verified reviews.

Just know that the system I’m about to share can work for ANYONE who follows it...

…we’ve had investors in their 80s succeed with it.

Nurses, school teachers, small business owners, engineers, doctors, we’ve seen it all and this system can work for ANYONE - experienced or not

These aren’t exceptions.

They’re what becomes possible when everyday investors get access to institutional-grade systems and a team that has their back.

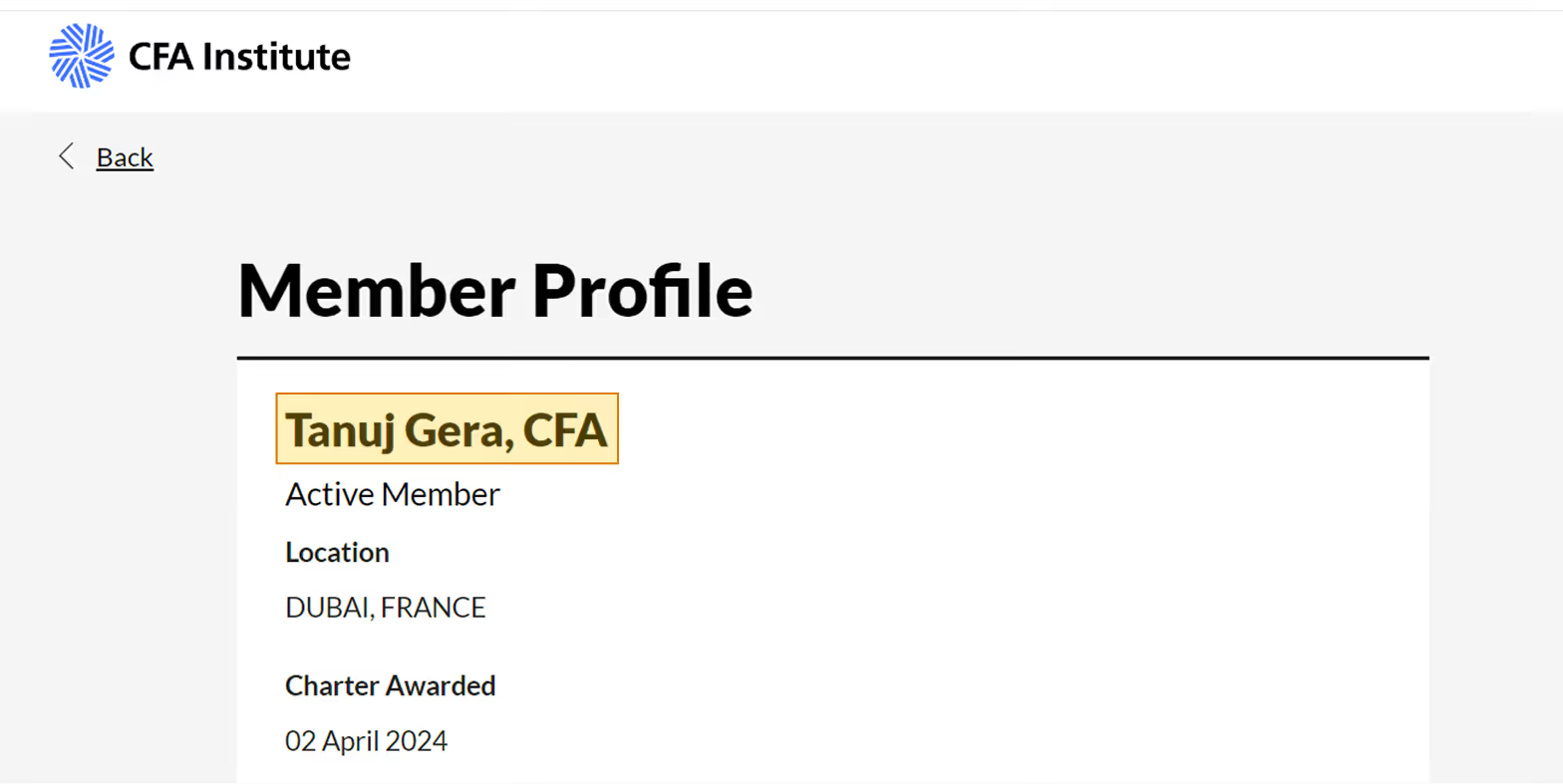

Now, the co-founder of Decentralized Masters is my colleague, Tan Gera

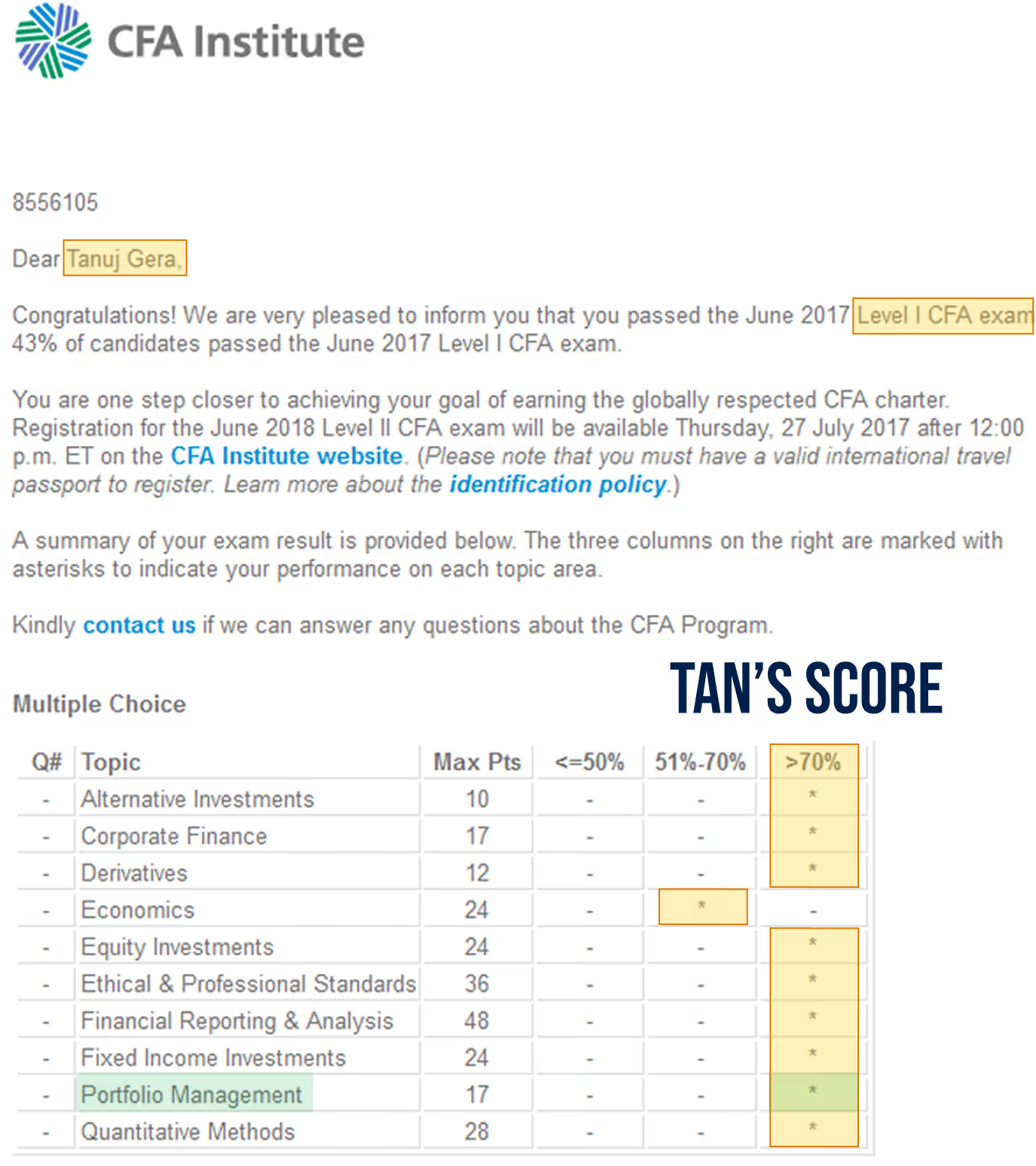

Tan is a CFA Charterholder with experience as an investment banker, private equity analyst, and hedge fund analyst.

The CFA program is considered to be the gold standard in the field of investment analysis.

The CFA program requires 900 hours of study over three years minimum… and has a 9% overall pass rate.

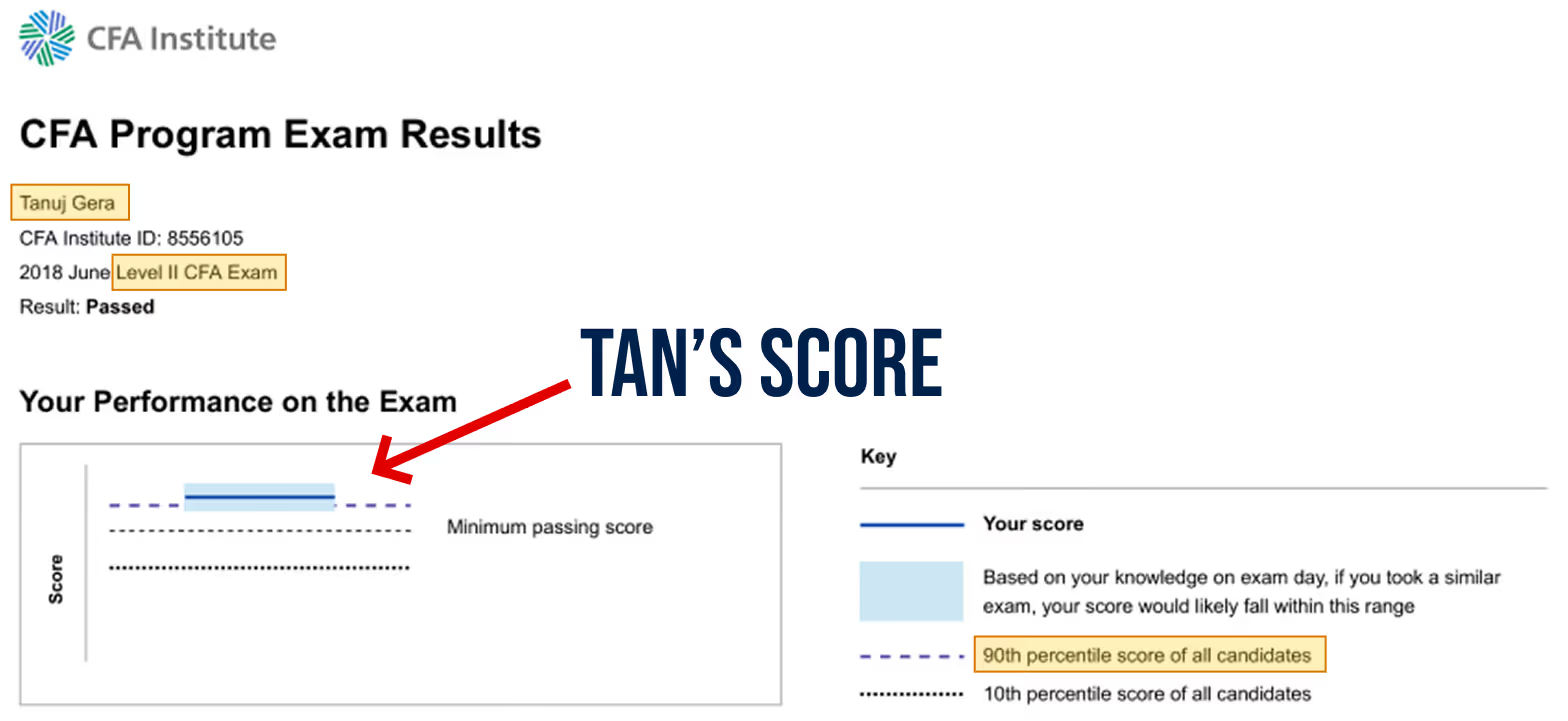

Tan ranked in the 90th percentile… meaning top 10% in the world… twice in a row on the Level 1 and Level 2 of the CFA Program exams - a designation held by only about 200,000 people in the entire world.

And among those charterholders? You'll find some of the most successful investors and financial minds in the world.

Mike Bloomberg… founder of Bloomberg… multi-multi-billionaire. He holds the CFA charter.

Howard Marks... co-founder of Oaktree Capital Management, the largest distressed securities investor worldwide.

Net worth: $2.2 billion.

CFA Charterholder since 1975.

These are people who committed years of their lives to mastering the science of investing.

Clearly, Tan is uniquely qualified at assessing the dire situation I’m about to share with you.

And when he first brought Project Ledgerfall to my attention, he said…

"Doc, this is the most dangerous financial development of our lifetime."

Coming from a man who spent years inside the system at the highest levels?

That got my attention.

So I dove into the research myself.

And what I found... once you know how to decode it... is deeply alarming.

Let me show you exactly what I saw.

The Three Phase Banking Control Plan

They Have Your Money Inside the System

Modern banking traces its roots back to Renaissance Italy.

The Medici family in Florence.

The original pitch was simple enough: give us your gold, we'll keep it safe in our vault, and we'll even pay you interest for the privilege of holding it.

It seemed like a fair deal. Banks used the deposits to facilitate trade.

The social contract was clear: banks were custodians. Protectors of your wealth.

But behind the scenes, the financiers discovered something far more lucrative than storage fees.

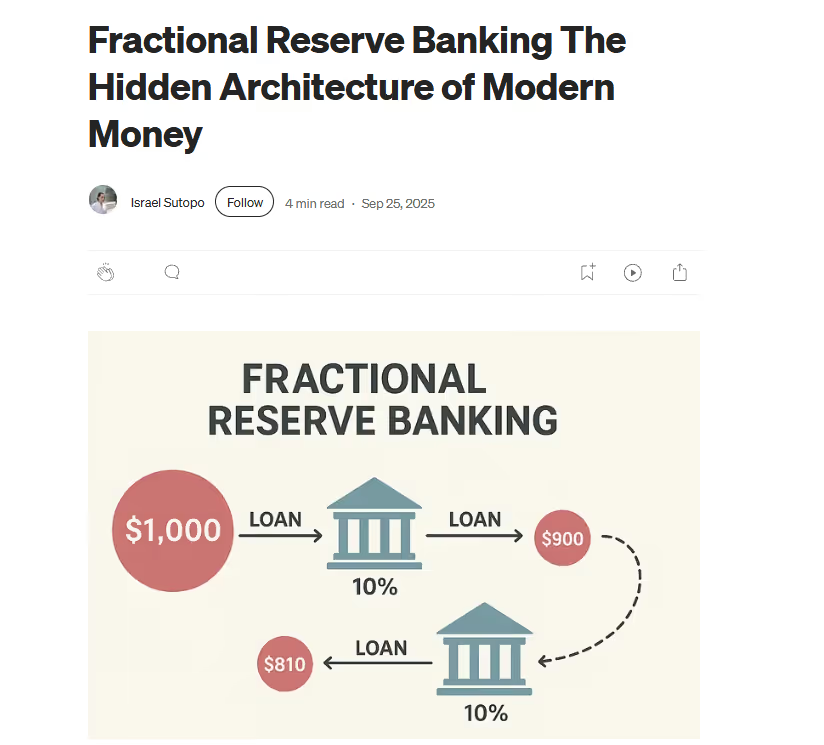

Fractional reserve banking.

Here's how it actually works: you deposit $1,000.

The bank keeps $100 in reserve and lends out the other $900.

That $900 gets deposited somewhere else, which lends out $810... and the cycle continues.

From your original $1,000 deposit, the banking system can create $10,000 or more in total loans.

They borrow your money at 0.5% interest.

They lend it out at 6% or more. And they pocket the difference, every single day, while you carry all the risk.

And if things go wrong? The pattern is always identical:

1987 - Black Monday. The Dow dropped 22.6% in a single day. Individual investors lost billions. The banks got rescued by the Fed.

2008 - The housing collapse. A $700 billion taxpayer bailout for the banks through TARP. Meanwhile, 10 million Americans lost their homes.

2020 - COVID. The Fed created over $4 trillion out of thin air in months. Big banks got unlimited liquidity. Small businesses closed permanently.

Every time, the pattern is the same: banks gamble, the system breaks, and taxpayers pay.

They Became Your Surveillance Agent

Starting in the 1970s, banks underwent a different kind of evolution.

One that tightened their grip even further.

They became surveillance agents for the state.

In 1970, Congress passed the Bank Secrecy Act, requiring banks to report "suspicious transactions" to the government.

Then came the Patriot Act after 9/11, which turbocharged the surveillance apparatus with Know Your Customer and Anti-Money Laundering requirements.

Over 11 million Suspicious Activity Reports were filed in 2025 alone.

Your bank now knows more about your life than your spouse does.

- Every transaction.

- Every purchase.

- Every transfer.

Documented, filed, and accessible to the government on request.

But even this wasn't enough. Because there was still one critical gap in their masterplan.

Cash.

When you hand someone a $100 bill, there's no record of that transaction. It's the last vestige of financial privacy in the modern world.

And banks and governments alike hate it.

Which is why they moved to Phase Three.

The Final Lock on the Cage - Project Ledgerfall

The architect of Phase Three was a man named Agustín Carstens.

From 2017 until July 2025, he was General Manager of the Bank for International Settlements - the BIS.

Think of the BIS as the central bank of central banks.

It coordinates monetary policy for 63 central banks worldwide, including the Federal Reserve, the European Central Bank, and virtually every other major monetary authority on the planet.

The BIS doesn't answer to voters.

It doesn't answer to Congress.

It operates largely outside public scrutiny…

It advises world leaders and sets the direction for global financial policy behind closed doors.

In October 2021, at the BIS Innovation Summit, Carstens made a statement that should have been front-page news everywhere.

He described a system where central banks would have "absolute control" over how money is used, and the technology to enforce that control.

Two years later, he laid out his vision for the Unified Ledger, one global digital infrastructure for all money and all assets.

Then in June 2025, Carstens handed the reins to his successor: Pablo Hernandez de Cos, the new General Manager of the Bank for International Settlements.

His job isn't just to upgrade the payment system. His job is to pull the trigger on the Unified Ledger.

One global platform. One digital infrastructure for all money, all assets, all financial activity - visible to central authorities in real-time. Your bank account. Your investments. Your credit card transactions. Your property records. All of it merged into one all-seeing system.

With what they call "programmable money." Currency with rules hard-coded at the software level.

Money that expires if you don't spend it fast enough.

Money that can only be spent in approved categories.

Money that can be switched off entirely, instantly, automatically, with no court order and no due process.

114 countries representing 98% of global GDP are already building versions of this system.

And the European Central Bank has already publicly agreed to roll out distributed ledger technology across member states in Q3 of 2026.

This is NOT a fringe theory.

This is NOT a conspiracy.

These are official publications from the BIS, the Financial Times, McKinsey, and the Federal Reserve itself. I'm reading their own documents back to you.

Still Not Sure? Let Me Show You What Happened in Canada…

Four years ago in Ottawa, thousands of truck drivers were peacefully protesting COVID-19 mandates.

The Canadian government invoked the Emergencies Act.

For the first time in Canadian history, they ordered banks to freeze the accounts of protestors and their supporters.

If you donated $50 to the convoy through a crowdfunding platform, your account could be frozen.

No court order. No due process.

One moment you had full access to your money.

The next moment, that access was gone.

This was Canada. A Western democracy with a Charter of Rights and Freedoms.

Central bank digital currencies would make this instant and automatic.

There would be no need for emergency orders.

The restrictions would be built directly into the code.

Nigeria tried it too.

When the government attempted to force adoption of their CBDC, the eNaira, and limited cash withdrawals to just $225 per week, the country erupted into protests.

The violence was real.

And the central bank is still looking for technology partners to try again.

These elites will not be denied. The infrastructure is being tested. The pilots are running. The legal frameworks are being built.

The only question is where will it happen next…?

“But That’s Canada. That’s Nigeria. That Won’t Happen Here.”

Fair point.

But let me show you something most Americans completely missed.

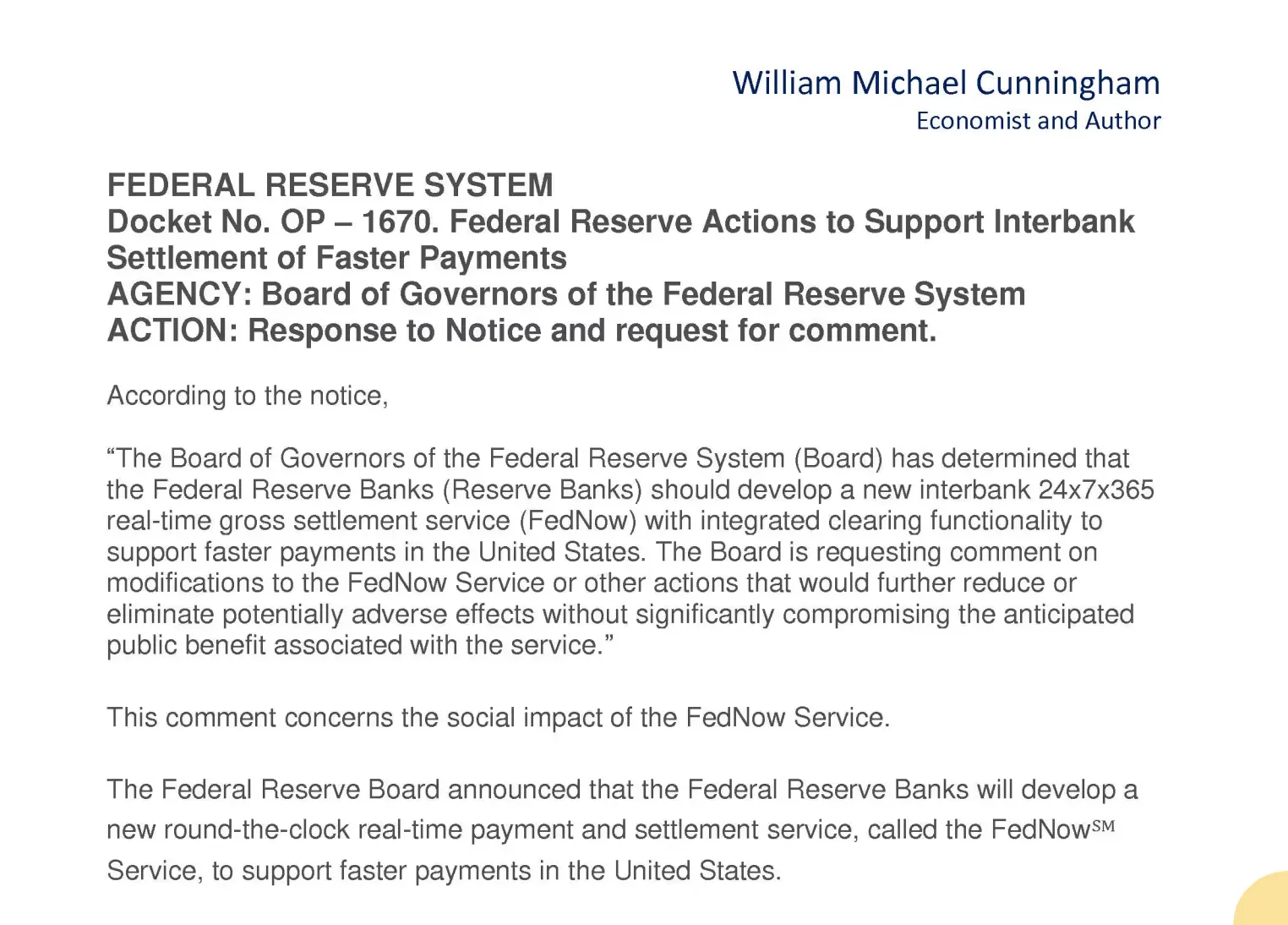

July 20th, 2023.

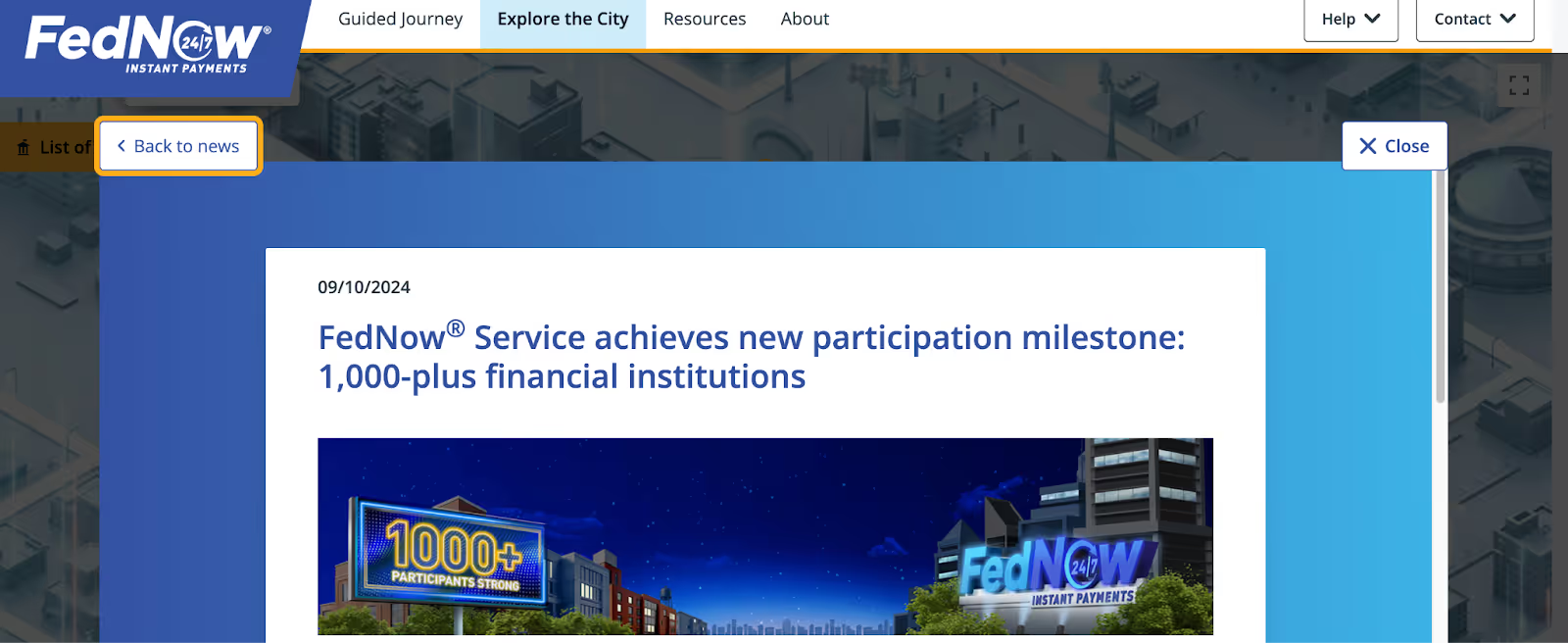

The Federal Reserve quietly launched something called FedNow.

No press conference.

No prime-time announcement.

No debate in Congress.

Just a quiet infrastructure rollout that got buried under the news cycle.

The Fed positioned it as simply a “money transfer system.”

A convenient way for banks to process payments faster. Nothing to worry about. Move along.

But insiders immediately started sounding the alarm.

Because lurking beneath its surface-level functionality,

FedNow looks exactly like the rails a digital dollar would be built on top of.

And this isn’t one analyst’s opinion.

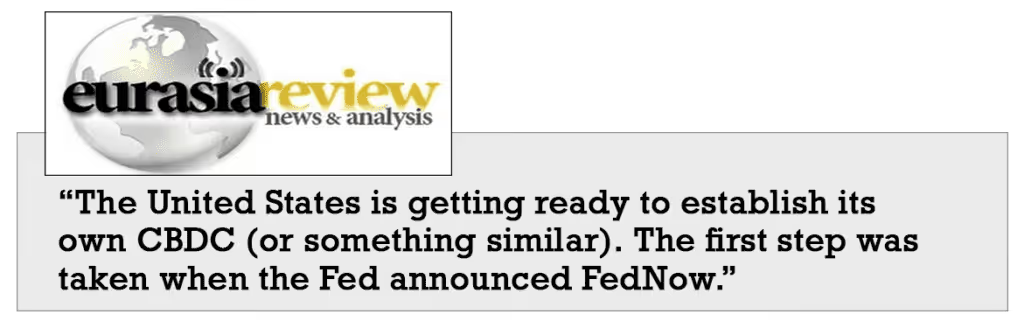

- The U.S. Gold Bureau called it out.

- CoinDesk called it out.

- Eurasia Review called it out.

All reaching the same conclusion independently: this is the first step.

The Trojan horse.

The infrastructure you build a CBDC on top of.

Those words matter. Real-time. Gross settlement. 24 hours a day, 7 days a week, 365 days a year.

That is not a modest upgrade to the ACH system.

That is the architecture of total financial visibility.

I’m not saying FedNow is the CBDC.

What I am saying is: it sounds exactly like the infrastructure one would be built on.

And the people who built it know precisely what they’re building.

Fast forward to today:

If you bank with any of them (and statistically there’s a strong chance you do), you may already be plugged into this infrastructure.

Now think about what happens if this infrastructure is extended to consumer accounts.

- They would have complete visibility of every dollar you spend.

- Instant freeze capabilities on any payment.

- Full control over who you can pay, when you can pay them, and what you’re allowed to buy.

And here’s what makes the American version of this uniquely dangerous: when Canada froze those accounts, some people moved money to American institutions.

When Nigeria restricted withdrawals, people found other currencies.

There was still somewhere to go.

When America does this - when, not if - there is nowhere left inside the system to run.

Because America IS the system.

The Fed has already published their roadmap document: Money and Payments: The U.S. Dollar in the Age of Digital Transformation.

The ECB launched their digital euro pilot in 2023.

China’s digital yuan processed $250 billion in transactions in 2023 alone.

105 countries are actively exploring CBDCs right now, with the Atlantic Council tracking 65+ in advanced phases.

Jamaica.

Nigeria.

India - processing 1 million CBDC transactions daily.

This is not a local problem.

It is a coordinated global financial shift.

And Bank of America, the second-largest bank in America, published a private research report to their institutional clients calling a U.S. digital dollar “inevitable,” with a timeline of 2025 to 2030.

We are already in that window.

The question is, what are you going to do about it?

THE ESCAPE ROUTE

Here's what gives me hope.

While de Cos builds his Unified Ledger, a parallel financial system has emerged that operates completely outside of it.

And the most powerful institutions in the world are already using it to position themselves.

I'm talking about stablecoins.

Stablecoins are digital dollars that live outside the banking system.

They're tokens designed to stay pegged to the dollar (one stablecoin equals one dollar) backed by real reserves of cash and short-term U.S. Treasuries.

These aren't experimental technology. Look at who's already using them:

These are the institutions that have spent the last century controlling the flow of money on this planet.

They see the same Unified Ledger plans you just read about.

They understand programmable, controllable money is the endgame.

And they're building infrastructure for a parallel financial system, while it's still legal to do so.

What Stablecoins Actually Allow You to Do

When you hold stablecoins in your own digital wallet, you're holding them in what's called self-custody.

Which means Chase can't freeze your account.

Bank of America can't restrict what you do with your money.

The Federal Reserve doesn't get a vote.

You control your money directly.

You can move it anywhere in the world, instantly, at any time of day or night.

- No wire delays.

- No weekend banking hours.

- No middleman taking a cut.

But here's the part that matters most, especially when banks are paying 0.5% while inflation runs at 3% or 4%:

You can earn real yield on your assets. Not the table scraps banks offer you. Actual returns that can outpace inflation - on the same dollars you'd otherwise leave sitting in a savings account doing nothing.

- You can hold stablecoins earning 4%, 6%, even 10% or more depending on your risk tolerance and the strategies you use.

- You can own tokenized gold, earning yield while preserving all the stability gold is known for, without storage fees, insurance costs, or liquidity problems.

- You can hold tokenized real estate that pays rental income and appreciation - with $100 instead of $100,000 - and sell your position in seconds instead of months.

Even stocks and bonds are being tokenized now.

You can hold the same assets you already trust and earn additional yield on top of dividends and interest just by holding them in tokenized form.

You know how banks take your deposits and lend them out to earn a spread?

They borrow your money at basically zero percent, lend it out at 6% or 7%, and pocket the difference while giving you table scraps.

With stablecoins, you can become the bank yourself.

You provide liquidity to platforms where traders and protocols need it.

Every time someone uses that liquidity, you collect a fee.

It's the same principle banks have been using for centuries, except now you're the one earning those returns instead of handing your capital to JPMorgan so they can profit from it.

Now, if you’ve heard about TerraUSD’s history, it’s fair to have some skepticism.

Yes, TerraUSD collapsed. And the story matters.

But TerraUSD was an algorithmic stablecoin. It wasn’t backed by real dollars or real reserves. It was backed by code and another token that could be printed out of thin air.

So when confidence broke, it death-spiraled to zero in 48 hours.

The stablecoins I’m describing - USDC, PayPal USD, and others like them - are reserve-backed 1-to-1 with actual U.S. dollars and U.S.

Treasuries, held in segregated accounts, audited daily by regulated institutions. Completely different animals.

That's the escape route.

It exists.

It works.

The only variable is time.

THE WINDOW IS CLOSING

The stablecoin landscape changes every month.

New platforms launch while others get shut down.

Yield opportunities rotate from one protocol to another overnight.

CBDC rollouts are accelerating across 114 countries, each one closing the escape window a little further.

You cannot set up a wallet in 2026 and walk away.

The rules of the game are changing while you're playing it.

And stablecoins - while legal today - will not remain outside the regulatory perimeter forever.

Every month that passes, the window to establish your position narrows.

That's why real-time intelligence matters right now.

Not just a one-time guide.

Not a course you take and forget.

Ongoing intelligence that tracks what's changing, which platforms are safe, where the yield actually is, and how close Phase Three is to becoming irreversible.

'BEAT BANKS WITH THE DEFI DOCTOR'

My team and I at Decentralized Masters built Beat Banks for exactly this moment.

It's your complete intelligence system for opting out of their control grid...

And becoming your own bank.

But let’s get one thing straight. This is about far more than one stablecoin strategy.

Beat Banks is a twice-weekly intelligence briefing built to help you move beyond the traditional banking system and start thinking like your own financial institution.

- That means learning how to protect your capital through self-custody.

- And how to position yourself across changing market conditions with a clear understanding of risk, mechanics, and execution.

- How to access yield opportunities across multiple blockchains.

- How to understand where liquidity is flowing.

This is not just about “earning yield.”

It’s about building the skills and systems to manage your capital productively in a decentralized world.

What You Get When You Activate Your Membership Today

Hedge funds pay firms like Chainalysis $50,000 a year to have this kind of analysis delivered to their managers' inboxes. Beat Banks delivers comparable intelligence, written specifically for serious individual investors, at a fraction of that cost.

The Team Behind Every Issue

And a full-time team of 35+ analysts who have been operating in DeFi for years, vetting platforms, tracking protocol risk, and surfacing opportunities with the same rigor we apply to our Mastermind community.

Inside Beat Banks, you're not getting one person's opinion.

You're getting the combined analysis of a team that has helped thousands of members navigate this space successfully.

What Members Are Saying

We've helped complete beginners set up self-custody wallets and start earning meaningful yield in their first month.

These are real results from real members. Not promises. Not projections. Results.

Choose Your Access to Beat Banks

Competitors charge over $1,000 per year for "institutional-grade financial intelligence" that still covers the old banking system and recommends stocks stuck in the same broken infrastructure you're trying to escape.

Beat Banks shows you how to opt out entirely.

We could easily justify charging $2,000 per year or more.

But I built this for everyday investors who have been locked out of financial freedom their whole lives.

The people who need this intelligence most are the ones who've never had access to it before.

Which is why a full annual membership is just $297 - a saving of $267 off the regular monthly price.

Or, if you want to try it first, you can activate a 7-day trial membership for just $1.

After your trial, membership continues at $47 per month. Cancel anytime.

The 30-Day No-Risk Guarantee

You have a full 30 days to read every briefing, work through the bonus reports, and evaluate this for yourself. If at any point you decide this isn't for you, email my team and we'll issue a full refund. No questions asked.

And you keep all four bonus reports regardless.

You risk nothing by saying yes today. You risk your financial options by waiting.

YOUR MEMBERSHIP OPTIONS

By now you already know something is wrong.

- You've felt it every time you check your savings account and see that 0.5% interest rate.

- You've felt it every time your dollar buys less than it did six months ago.

- You've felt it watching the institutions quietly position themselves while telling you everything is fine.

The system isn't working for you anymore.

The only question is whether you're going to do something about it…

Or keep waiting and hoping it gets better on its own.

De Cos is moving forward whether you act or not.

The Unified Ledger is being built. The BIS is coordinating with 114 countries.

The pilot programs are running.

And every month that passes, the infrastructure gets more sophisticated and the exits get harder to find.

Right now, you still have a choice.

You can stay inside a system being redesigned to monitor every dollar you spend, profile every transaction you make, and restrict your financial freedom based on criteria you'll never fully understand.

Or you can step into a parallel system that still respects your sovereignty.

A system where you hold your own assets, earn real yields instead of accepting scraps, and where no bank can freeze you out and no government can program your money.

The window is open right now.

I can't tell you how long it stays that way.

Click the button below. Activate your Beat Banks membership. Get instant access to all four special reports. Start reading.

Do it before de Cos closes the door.

Do it while stablecoins are still legal to hold in self-custody.

Do it before the Unified Ledger becomes the only option.